Introduction: Making Insurance Accessible to All

Life Insurance Corporation of India (LIC) has long been committed to financial inclusion across India’s diverse socioeconomic landscape. While traditional insurance policies often remain out of reach for many low-income families and rural communities due to high premiums and complex terms, LIC’s micro-insurance products are specifically designed to bridge this gap. These affordable, simplified policies provide essential financial protection for the economically vulnerable sections of our society.

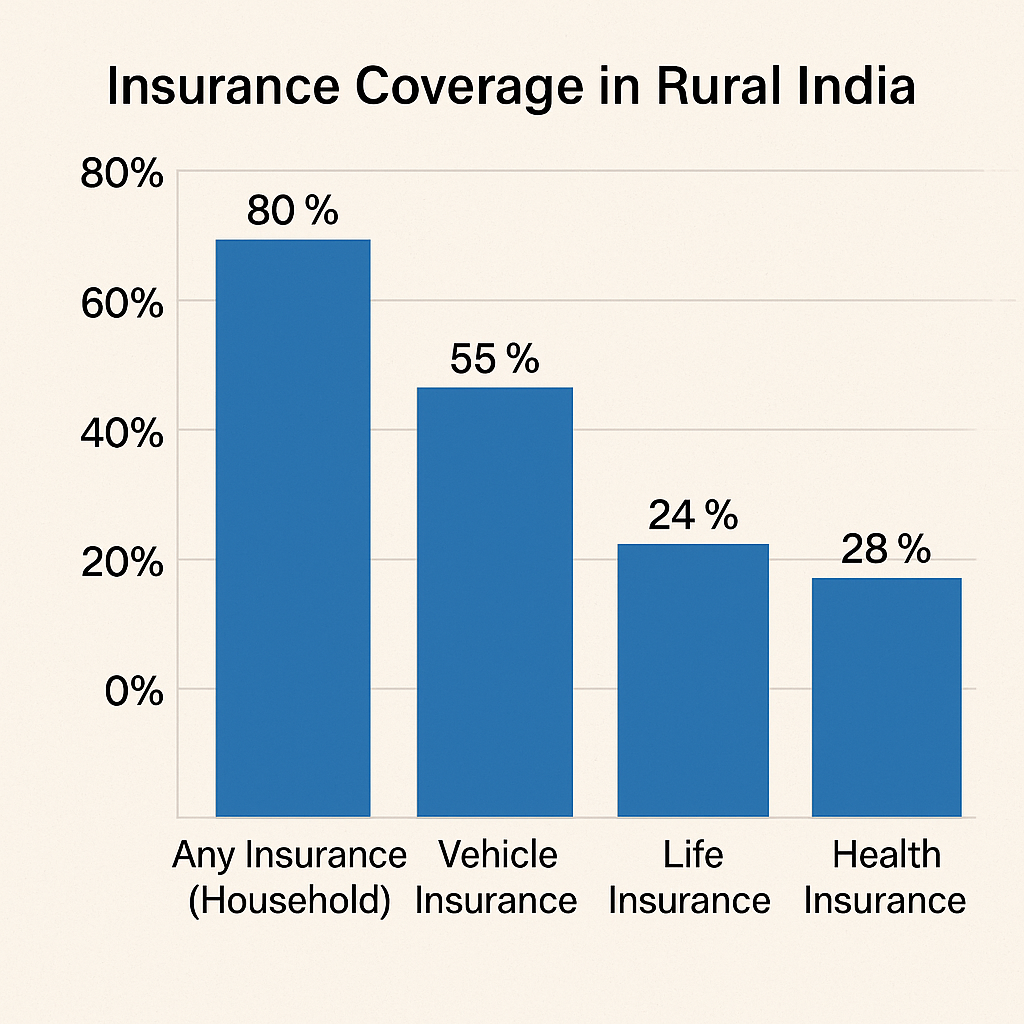

According to a recent report by the Insurance Regulatory and Development Authority of India, only 3.7% of India’s rural population has adequate life insurance coverage, highlighting the critical need for accessible insurance solutions.

What is Micro-Insurance?

Micro-insurance refers to insurance products with low premiums, simplified terms, and modest coverage amounts tailored to meet the unique needs of economically disadvantaged individuals and families. According to the IRDAI (Insurance Regulatory and Development Authority of India), micro-insurance products have specific coverage limits and are designed for financial inclusion.

The primary features of micro-insurance include:

- Low premium amounts (often starting from ₹100-200 annually)

- Simplified documentation and claim processes

- Smaller coverage amounts suited to actual needs

- Limited exclusions and conditions

- Flexible payment options

For more details on how micro-insurance differs from traditional insurance, you can refer to our previous article on Understanding Different Types of Insurance Products in India.

LIC’s Micro-Insurance Portfolio

LIC offers several micro-insurance products designed to meet the specific needs of low-income communities:

1. LIC’s Bhagya Lakshmi Plan

This plan provides financial security to the family of female policyholders in case of unfortunate events while offering maturity benefits. Key features include:

- Ages: 18-45 years

- Policy Term: 5-15 years

- Minimum Sum Assured: ₹5,000

- Maximum Sum Assured: ₹30,000

- Premium payment modes: Yearly, Half-yearly, Quarterly, or Monthly

The policy provides a death benefit equal to the sum assured plus vested bonuses, while the maturity benefit equals the sum assured plus vested bonuses if the policyholder survives the policy term.

2. LIC’s Jeevan Mangal Plan

This is a micro-insurance endowment assurance plan providing financial protection against death throughout the term of the plan along with a maturity benefit.

- Ages: 18-60 years

- Policy Term: 5-15 years

- Minimum Sum Assured: ₹10,000

- Maximum Sum Assured: ₹50,000

- Premium Payment Options: Single premium or regular payments

The unique aspect of this plan is its accessibility for informal workers without steady income streams, allowing them to secure insurance protection with minimal documentation. Learn more about endowment plans in our guide to Choosing the Right Insurance Plan for Your Family.

3. LIC’s Jeevan Shagun Plan

This plan combines savings and insurance protection:

- Ages: 18-60 years

- Policy Term: 5-15 years

- Minimum Sum Assured: ₹5,000

- Maximum Sum Assured: ₹30,000

- Premium Payment Flexibility: Quarterly, Half-yearly, or Annual

Perfect for seasonal workers or agricultural laborers who may not have regular monthly income but can pay premiums after harvest seasons. For comparison with other savings options, see our article on Agricultural Workers’ Financial Planning.

The Impact of Micro-Insurance on Rural Communities

Micro-insurance plays a crucial role in breaking the cycle of poverty in rural India. When a family’s primary earner passes away without insurance protection, the family often falls deeper into poverty. Even modest coverage amounts of ₹10,000-50,000 can:

- Cover immediate funeral expenses

- Provide time for the family to adjust financially

- Prevent emergency asset liquidation at unfavorable terms

- Support education continuation for children

- Prevent debt traps from high-interest emergency loans

According to a 2023 study by the National Bank for Agriculture and Rural Development (NABARD), families with micro-insurance coverage were 42% less likely to remove children from school following the death of a primary earner compared to uninsured families.

How to Apply for LIC’s Micro-Insurance

The application process has been simplified to increase accessibility:

- Minimal Documentation: Usually just Aadhaar card or voter ID, with relaxed KYC norms

- Local Assistance: Applications through LIC agents, Common Service Centers (CSCs), or banking correspondents

- Digital Options: Mobile applications in regional languages

- Group Enrollment: Community-based enrollment through self-help groups and microfinance institutions

For assistance locating your nearest LIC office or agent, use the official LIC branch locator.

Claim Settlement Process

LIC has streamlined the claim settlement process for micro-insurance products:

- Simplified Documentation: Death certificate and proof of identity are usually sufficient

- Local Verification: Village authorities can often verify claims

- Faster Processing: Claims typically processed within 7-15 days

- Direct Transfer: Benefits transferred directly to beneficiary bank accounts

For detailed steps on filing insurance claims, refer to our comprehensive guide on How to File Insurance Claims in India.

Challenges and Solutions

Despite their benefits, micro-insurance products face challenges in reaching their target audience:

Awareness Gap

Many potential beneficiaries are unaware of micro-insurance options. LIC addresses this through:

- Village-level awareness campaigns

- Partnerships with Panchayats and local governance bodies

- Insurance education through street plays and community meetings

- Utilizing local dialect in promotional materials

For more on financial literacy initiatives, see our article on Financial Education in Rural India.

Trust Issues

Building trust in insurance among communities with limited financial literacy is challenging. LIC’s approach includes:

- Transparent communication about benefits and limitations

- Community testimonials from beneficiaries

- Involvement of respected community leaders as advocates

- Public claim settlement events to demonstrate reliability

Future of Micro-Insurance in India

The micro-insurance market in India is expected to grow significantly as financial inclusion initiatives expand. Key trends include:

- Digital Integration: Mobile-based enrollment, premium payment, and claim filing

- Expanded Coverage: New products covering health, crop, and livestock

- Bundled Services: Insurance combined with savings and credit products

- Data Analytics: Better risk assessment for rural and low-income segments

For more insights on the future of insurance in India, read our analysis of Digital Transformation in Indian Insurance Sector.

Conclusion: Financial Security for All

LIC’s micro-insurance products represent a crucial step toward universal financial protection in India. By making insurance accessible and affordable for low-income families and rural customers, these products help build financial resilience among the most vulnerable sections of society.

For those looking to secure their family’s future without straining their limited financial resources, LIC’s micro-insurance plans offer a viable path to protection. These products demonstrate that financial security need not be a privilege of the affluent but can be accessible to all segments of society.

For personalized advice on selecting the right micro-insurance product for your needs, explore our Insurance Plan Selection Guide.

FAQs About LIC Micro-Insurance

Q1: Can I buy micro-insurance policies online? A: While some aspects of the application process are being digitized, most micro-insurance policies are sold through agents, banking correspondents, or Common Service Centers (CSCs) to provide personal assistance during enrollment.

Q2: Are the claim settlement procedures complicated? A: No, LIC has significantly simplified claim settlement procedures for micro-insurance policies, requiring minimal documentation and offering local assistance.

Q3: Can I convert my micro-insurance policy to a regular policy later? A: Most micro-insurance policies don’t offer direct conversion options, but policyholders can apply for regular policies as their financial situation improves.

Q4: Are there any tax benefits available on micro-insurance premiums? A: Yes, premiums paid for LIC micro-insurance policies qualify for tax deduction under Section 80C of the Income Tax Act, though many policyholders may not have taxable income.

Q5: How do premium payment schedules accommodate irregular income patterns? A: LIC offers flexible payment options including quarterly half-yearly, and annual premium modes to accommodate seasonal income patterns common among agricultural workers and daily wage earners.

")